by Matt, on 20 Nov 2019

Today, SPT offers you a whistle-stop tour of the investor trail. Beginning with your trusted friends and family and winding our way through venture capital and private equity, we’ll hit the highlights and idiosyncrasies of these potential sources of funding.

You might be wondering what that’s got to do with ‘new clothes’. Our catchy headline is a hat-tip to 16th century Italy where the Latin word investīre, which originally meant ‘to clothe in’, acquired its new sense of injecting capital and clothing that capital with new value. (Sorry if you were hoping to read a post about the latest trends in hoodies and sustainably made sneakers).

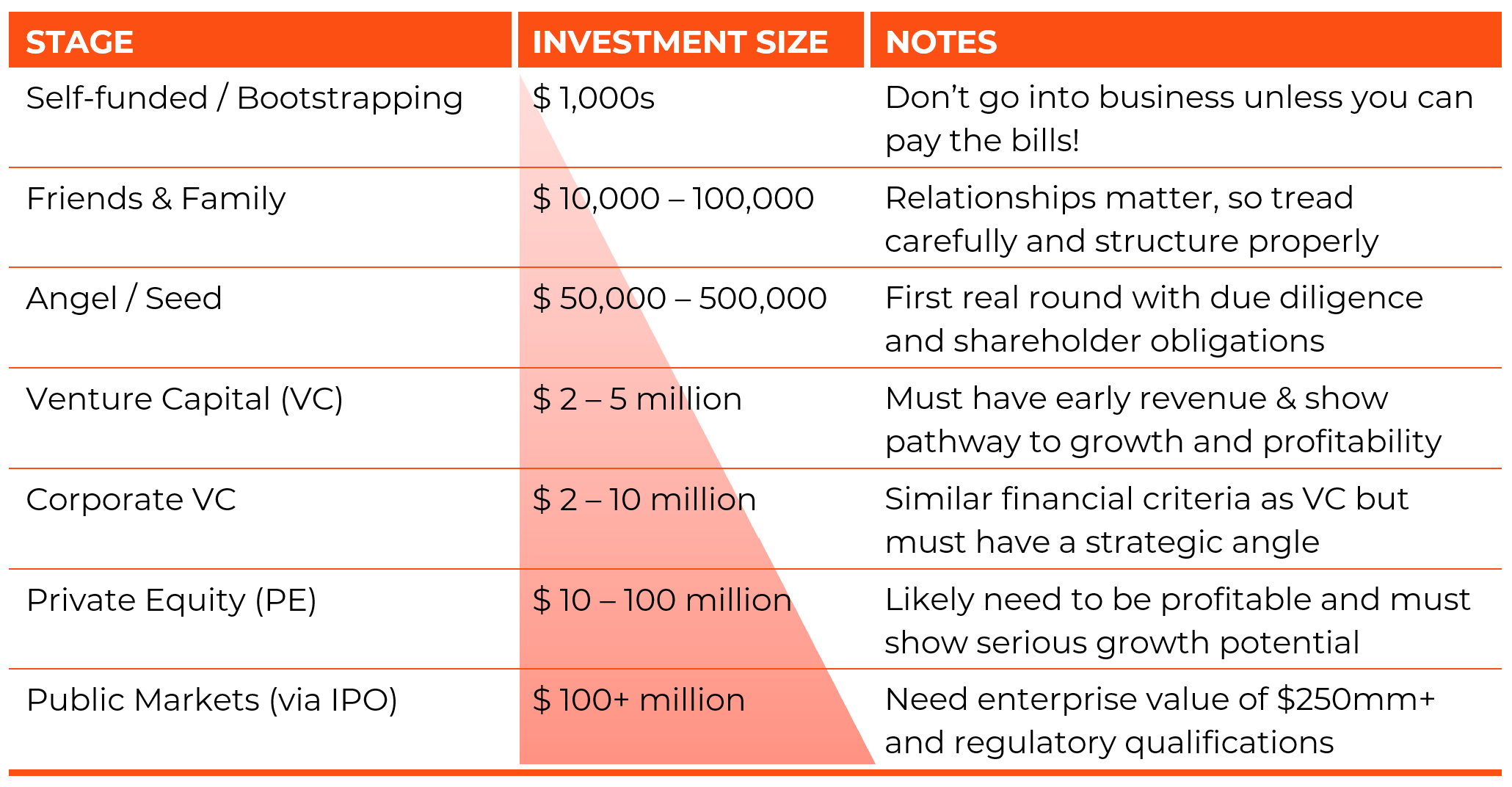

Let’s set the scene. You’re an aspiring CEO with an idea that’s itching to find its way from your bar napkin sketch into the hands of a million users. A quick check of the bank app confirms that no financial miracle has happened overnight; you have a few thousand dollars in personal savings, which isn’t going to pay the bills for very long if you pursue this idea full time.

Time to sell your idea, quite literally, to others who do have money and would surely like to give you some in return for a share in this unicorn ride to fame and riches.

FRIENDS + FAMILY

After exhausting their personal funds, the first group of potential investors that most entrepreneurs turn to is friends and relatives. Although it’s still incumbent on the entrepreneur to convince them that their idea represents a worthwhile investment, pre-existing levels of trust with friends and family makes this easier.

Unless you’re fortunate enough to come from a wealthy family or to hang out with financially secure friends, the total size of a friends and family investment round is usually only a few tens of thousands of dollars. However, this can go a long way when the venture is just getting started and carries minimal overhead.

It’s wise to seek legal advice and set things up carefully before inviting your BFFs to buy into the company. Mistakes made at this point can lead to unwelcome delays and restructuring costs if your business is a success and you want to raise institutional investment later.

You should also consider how a failure of the business would affect your relationships with these individuals. Burning through your friends’ life savings doesn’t usually go down too well, so make sure they only invest capital that they can truly afford to lose.

ANGEL INVESTORS

An angel investor (a.k.a. seed investor or angel funder) is typically a high net worth individual who provides funding for startups in exchange for an ownership stake in the company.

While angel investors are sometimes found among the entrepreneur's friends and family, organized angel networks exist in many cities and in affiliation with some universities.

For example, the Houston Angel Network, one of the most active groups of this type in the country, coordinates the opportunity screening, due diligence, and investment activities of over a hundred qualified investors within the Greater Houston area.

Angel investors are usually the first source of capital an entrepreneur will tap into after the company’s needs exceed personal financial resources and those of the friends and family network.

Seed funding from angel investors typically ranges from $50,000 to $500,000, with larger amounts often invested in multiple tranches.

SUPER ANGELS

A super angel investor tends to be a serial investor in early stage businesses who is financially more sophisticated or more well-connected in business circles than other members of the angel community.

The term doesn’t necessarily imply that the super angel has access to more funds or writes bigger checks than a regular angel, although either can certainly be the case.

If you can identify the super angels in your geographic region or business domain, they can be valuable points of contact for more in-depth business plan reviews or as a lead investor if you plan to raise an amount that will require the participation of multiple sources of capital.

VENTURE CAPITAL

Venture capital is a form of private equity financing that investors provide to startup companies and small businesses that they believe have long-term growth potential.

The capital is invested on the understanding that there is still a substantial element of risk involved, which may be both technical and commercial in nature.

Venture capital generally comes from firms that specialize in building portfolios of higher risk investments. Even though a relatively small percentage of their investments will be successful, VC firms generate a superior rate of return by investing at an early stage when the target companies’ valuations are still quite low.

Many venture capital firms limit their investments to companies that have begun generating revenue. While they might not yet be profitable, showing early customer traction becomes an important screening criterion, as does having a clear business plan that anticipates a high rate of growth and profitability within the investor’s time horizon.

Since most investment funds have a ten-year life, after which the limited partners expect to harvest their returns, the time horizon within which any given investment will be expected to fulfill its potential is typically 4-7 years.

The size of venture capital investments varies widely across locations and industries. West Coast VCs investing in technology startups might write checks in the tens of millions of dollars, while Austin or Houston based funds investing in energy or healthcare ventures might put in a more modest $2-5 million.

CORPORATE VENTURE CAPITAL

Corporate venturing is the practice of directly investing corporate funds into external startup companies.

Many large corporations engage in some form of CVC investment to help incubate and accelerate business ideas and technologies that could increase the value of their wider enterprise, either as future suppliers or takeover targets.

Their investment criteria are therefore both financial and strategic in nature. Even an opportunity that’s a financial no-brainer won’t attract funding unless it could have a disproportionate (i.e. strategically significant) impact on the corporation’s business.

CVC plays an important role in funding technically risky ventures that external investors, lacking the domain expertise of a large corporation, cannot properly evaluate or accommodate within their risk-based portfolios.

If your business concept is aimed at disrupting a sector where large corporations play, their internal VC groups could be a viable source of capital for you.

However, be sure to ask what additional value they will bring to the table. One of the advantages of working with a corporate investor should be their ability to organize proof of concept trials and early product adoption. Securing their commitment to provide these otherwise hard-to-come-by access points can make their investment significantly more important and valuable than funding from a financial institution.

PRIVATE EQUITY

Private equity (PE) consists of capital funds that directly invest in private companies (i.e. those that are not listed on a public exchange) or that buy out public companies, delisting the public equity and taking the company private.

Common investment strategies employed by PE funds include growth capital and leveraged buyouts, as well as late-stage venture capital, distressed investments, and mezzanine capital (more on that, below).

Most private equity funds will only invest in companies that are generating free cash flow (i.e. they are profitable) and that have significant near-term growth potential.

Since they are putting significantly more capital to work than most VC funds, PE investors will generally want to invest tens to hundreds of millions of dollars in a single company.

SINGLE FAMILY OFFICE

Traditionally, a Single Family Office (SFO) is a business run by and for a single family, managing wealth that has often been accumulated over generations. Several thousand SFOs are in operation across the United States.

Because each SFO is driven by the needs and preferences of the underlying family, there is no standard for how they are structured or operated. Some employ a small staff that focuses exclusively on investing while others are large organizations that manage numerous business relationships and perform a broad range of services.

In recent years, small groups of like-minded families have joined forces to create Multi-Family Offices, with a view to sharing infrastructure and overhead costs. This affords them an opportunity to invest more broadly, with an eye toward profit and growth.

SFOs tend to engage in fewer, longer-term investment relationships because their objective is wealth management rather than outsized near-term returns.

If you are looking for ‘patient capital’ to fund your business – perhaps because you expect to take several years to develop and commercialize your product - and can demonstrate that the technical and commercial risks are low, then contacting SFOs for investment could be worthwhile.

MEZZANINE CAPITAL

Mezzanine financing is a hybrid between debt and equity where the lender retains the right to convert the loan into an equity interest if the company defaults on its payments.

Mezzanine loans often come with interest rates as high as 20-30% and are most commonly used for the expansion of established companies rather than for startup or early stage businesses.

THE PUBLIC MARKETS

In the public markets, companies sell shares to the general population. These shares can then be bought, sold or traded on a stock exchange.

The concept dates back to the 17th century, when the Dutch East India Company became the first company to list its shares. This laid the foundation for today’s global equities trade where thousands of companies make shares and financial products available to the public.

Listed companies must follow reporting requirements laid down by local financial authorities (for example, the United States’ Securities and Exchange Commission), their shareholders, and other interested parties. As a result, public companies are subject to much more public scrutiny than private companies.

A company begins trading its shares through an Initial Public Offering (IPO). This process, known as ‘going public’, allows the market to determine the value of the company as its stock price fluctuates in response to financial performance, market sentiment, and macroeconomic factors.

Going public is an opportunity for the company to access much larger amounts of capital than by simply reinvesting its profits or tapping into private investment.

How big must a company be in order to stage a successful IPO? That’s a matter of debate but we reckon its enterprise value should be above $250 million.

IN THE MIRROR

Here’s a quick summary of the different types of ‘new clothes’ we covered:

Is fundraising an upcoming milestone for you? Check out our Seed Funding or Venture Funding.